Get summaries, questions, answers, solutions, notes, extras, PDF and guide of Class 11 (first year) Economics textbook, chapter 6 Concepts of Costs, which is part of the syllabus of students studying under AHSEC/ASSEB (Assam Board). These solutions, however, should only be treated as references and can be modified/changed.

If you notice any errors in the notes, please mention them in the comments

Summary

The chapter discusses different concepts of cost, including the cost of production, short-run costs, and long-run costs. It begins by explaining the cost of production as the total expenses incurred by a firm to purchase inputs. These include explicit costs, which are actual payments made to suppliers, and implicit costs, which refer to the value of resources owned by the firm, such as the rent of a building owned by the producer. The sum of both explicit and implicit costs makes up the total economic cost.

In the short run, some costs remain fixed, while others can vary. Fixed costs, such as rent, do not change with output and are incurred even if no production occurs. Variable costs, like wages or raw material expenses, change directly with the level of production. These costs together form the total cost, which is the sum of fixed and variable costs.

The chapter explains the behavior of these costs using tables and graphs. Fixed costs remain constant regardless of output, while variable costs increase as production increases. The total cost curve follows the pattern of the variable cost curve, with the vertical distance between them representing the fixed costs.

Average costs are also discussed, including average fixed cost (AFC), average variable cost (AVC), and average total cost (ATC). The AFC curve slopes downward because fixed costs are spread over an increasing number of output units. The AVC and ATC curves are U-shaped, first decreasing due to increasing returns to variable factors and later rising as diminishing returns set in.

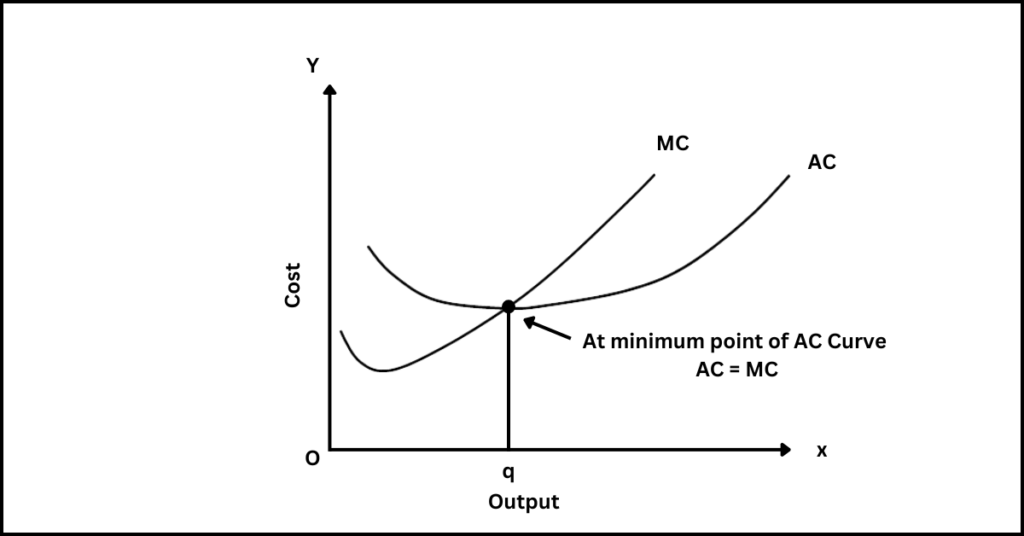

Marginal cost (MC) is the additional cost incurred by producing one more unit. The marginal cost curve is also U-shaped, initially decreasing and then increasing. It intersects the AVC and ATC curves at their lowest points.

In the long run, all costs are variable. The long-run average cost curve (LAC) is derived from various short-run average cost curves and is U-shaped due to economies and diseconomies of scale. It reflects the least cost for producing each level of output. The long-run marginal cost curve (LMC) behaves similarly to the short-run marginal cost curve, with both curves following a U-shape.

Textbook solutions

Very Short Answer Type Questions

1. Define economic costs.

Answer: Economic cost is the sum total of actual money expenditure on inputs (i.e., explicit costs) and the estimated value of self-supplied inputs by the owner (i.e., implicit costs) and normal profits.

2. What are implicit costs?

Answer: Implicit costs refer to the estimated (or imputed) value of inputs supplied by the owner of the firm, such as imputed salary of the owner or imputed rent of the building owned by the firm.

3. Give two examples of explicit costs in a tailoring shop.

Answer: Two examples of explicit costs in a tailoring shop are expenditure on the purchase of fabric and payment of wages to hired workers.

4. Give two examples of implicit costs of a firm.

Answer: Two examples of implicit costs of a firm are the imputed salary of the owner and the imputed rent for the use of a building owned by the firm.

5. What is meant by fixed cost?

Answer: Fixed cost refers to the cost that does not change with the level of output. Fixed costs remain constant regardless of the amount of goods produced. Examples include rent of the building and interest on loans.

6. What is meant by variable cost?

Answer: Variable cost refers to the cost that varies with the level of output. It changes as the quantity of goods produced increases or decreases. Examples include costs of raw materials and wages of temporary staff.

7. Give two examples of fixed costs.

Answer: Two examples of fixed costs are the rent for the building and the salaries of permanent staff.

8. Give two examples of variable costs.

Answer: Two examples of variable costs are the cost of raw materials and wages paid to casual or temporary workers.

9. What is the shape of TFC curve?

Answer: TFC curve is a horizontal straight line.

10. What is the shape of TVC curve?

Answer: TVC curve is initially concave downward and then concave upward.

11. What are the main constituents of total costs? Name them.

Answer: The main constituents of total costs are total fixed cost and total variable cost.

12. What is the difference between TC and TFC called?

Answer: The difference between TC and TFC is called total variable cost (TVC).

13. What is average cost?

Answer: Average cost is the total cost per unit of output.

14. Give the formula of calculating average cost.

Answer: The formula for calculating average cost is AC = TC/Q, where AC is average cost, TC is total cost, and Q is the quantity of output.

15. Define marginal cost. With the help of an example show how marginal cost can be obtained from total cost.

Answer: Marginal cost is defined as the increase in total cost when one extra unit of output is produced. For example, if the total cost of producing 5 units of a commodity is ₹36, and it goes to ₹45 when 6 units are produced, the marginal cost of the 6th unit is ₹9 (₹45 – ₹36).

16. Do fixed costs affect marginal cost?

Answer: No, fixed costs do not affect marginal cost.

17. What would you say about the average cost of a firm if the marginal cost of production is less than the average cost?

Answer: If the marginal cost of production is less than the average cost, then the average cost will be falling.

18. Can average cost fall when marginal cost is rising?

Answer: Yes, average cost may fall even when marginal cost is rising, as long as the marginal cost is still below the average cost.

19. Define average fixed cost.

Answer: Average fixed cost (AFC) is the per unit fixed cost of output. It is calculated as the ratio of total fixed cost to the output.

20. Fill in the blanks in the following:

(i) TC = TFC + _____

(ii) _____ = TVC/Q

(iii) AFC + AVC = _____

(iv) _____= ΔTC/ΔQ

Answer:

(i) TC = TFC + TVC

(ii) AVC = TVC/Q

(iii) AFC + AVC = ATC

(iv) MC = ΔTC/ΔQ

21. How does the AFC curve slope?

Answer: The AFC curve slopes downwards because as output increases, average fixed cost falls continuously.

22. How does the AVC curve slope?

Answer: The AVC curve first slopes downward as output increases, reflecting increasing returns, and then slopes upward after reaching a minimum point, due to diminishing returns.

23. Define (a) long run average cost and (b) long run marginal cost.

Answer: (a) Long-run average cost (LRAC) refers to the minimum achievable cost per unit of output when all factors of production are variable in the long run.

(b) Long-run marginal cost (LRMC) refers to the change in total cost that results from producing one more unit of output in the long run when all inputs are variable.

Short Answer Type Questions

1. Define fixed costs of a firm. Give examples.

Answer: Fixed costs are the costs that a firm incurs to employ fixed inputs or factors (e.g., plant and equipment, building, etc.). These costs do not vary with the level of output produced. Fixed costs are incurred even if the output is zero, and they remain constant irrespective of the level of production. Examples of fixed costs include the rent of a factory building and the salaries of permanent staff.

2. Define variable costs of a firm. Give examples.

Answer: Variable costs are the costs incurred on inputs that vary with the level of output. These costs increase as the output increases and decrease when the output decreases. Variable costs are directly associated with production and become zero when no output is produced. Examples of variable costs include payments for raw materials and wages for temporary staff.

3. Distinguish between fixed cost and variable cost. Give two examples of each.

Answer:

Fixed costs:

- Fixed costs do not change with the level of output. They remain the same even if output is zero.

- Fixed costs are unavoidable in the short run.

Examples: Rent for the factory, salary of permanent staff.

Variable costs:

- Variable costs change with the level of output. They increase as output increases and decrease as output decreases.

- Variable costs can be avoided if no output is produced.

Examples: Payment for raw materials, wages for casual workers.

4. Can average fixed cost (AFC) be zero? Explain the shape of AFC curve.

Answer: Average fixed cost (AFC) can never be zero because fixed costs are constant, and AFC is derived by dividing the total fixed cost by the output. As long as the output is positive, AFC will always be positive, though it decreases as output increases. The AFC curve is a rectangular hyperbola because the total fixed cost remains the same while the output increases, leading to a continuously decreasing AFC.

5. Draw ATC, AVC and MC curves in a single diagram.

Answer: [The document does not provide the actual diagram, but the required curves, ATC (Average Total Cost), AVC (Average Variable Cost), and MC (Marginal Cost), are all U-shaped curves. The MC curve typically intersects both the ATC and AVC curves at their respective minimum points. This behavior is due to the law of diminishing returns.]

6. Do AVC curve and ATC curve intersect? State reasons for your answer.

Answer: No, the AVC curve and ATC curve do not intersect. This is because the ATC curve is the summation of the AVC and AFC curves. Since AFC is always positive, ATC will always be higher than AVC by the amount of AFC, and therefore, they cannot intersect.

7. Why is AC curve U-shaped?

Answer: The average cost curve (AC) is U-shaped because of the law of variable proportions. Initially, as the level of output increases, the firm experiences increasing returns to a factor, which leads to a fall in the average cost. After a certain point, however, diminishing returns to a factor set in, and the average cost begins to rise. Hence, the AC curve is U-shaped.

8. Describe the relationship between AVC and MC.

Answer: The relationship between average variable cost (AVC) and marginal cost (MC) is as follows:

- When AVC is falling, MC is less than AVC.

- When AVC reaches its lowest point, MC equals AVC.

- When AVC starts rising, MC is greater than AVC.

9. The total cost of a firm is 100 when it produces 15 units of output. If the level of output increases to 30 units, what will be the fixed cost in the short run? Explain. (AHSEC Question Bank)

Answer: The fixed cost will remain the same in the short run, irrespective of the output level. Therefore, if the total cost of producing 15 units is ₹100, the fixed cost will remain ₹100 even if the output increases to 30 units. This is because fixed costs do not change with the level of output in the short run.

10. State the behaviour of Total Variable Cost. Draw Total Variable Cost, Total Cost and Total Fixed Cost Curves in a single diagram.

Answer: The behaviour of Total Variable Cost (TVC) is as follows:

- Initially, total variable cost increases at a decreasing rate as output increases.

- After a certain point, TVC increases at an increasing rate.

(Total Variable Cost, Total Cost, and Total Fixed Cost Curves should be drawn as per standard economic diagrams, with Total Fixed Cost remaining constant, Total Variable Cost increasing, and Total Cost being the sum of both.)

11. State whether the following statements are true or false. Give reasons.

(i) Average cost falls only when marginal cost falls.

(ii) The difference between average total cost and average variable cost is constant.

(iii) As output is increased, the difference between average total cost and average variable cost falls and ultimately becomes zero.

Answer: (i) False: Average cost falls when marginal cost is less than average cost, not necessarily when marginal cost falls.

(ii) False: The difference between average total cost and average variable cost is the average fixed cost, which decreases as output increases.

(iii) False: The difference between average total cost and average variable cost is the average fixed cost, which decreases but never becomes zero.

12. State whether the following statements are true or false. Give reasons.

(i) The difference between average total cost and average variable cost decreases with a decrease in the level of output.

(ii) When marginal cost rises, average cost will also rise.

Answer: (i) False: The difference between average total cost (ATC) and average variable cost (AVC) is the average fixed cost (AFC). AFC increases as the level of output decreases, so the difference between ATC and AVC actually increases with a decrease in output.

(ii) False: When marginal cost (MC) rises, average cost (AC) will rise only if MC is greater than AC. If MC is still less than AC, AC will continue to fall even though MC is rising.

Long Answer Type Questions

1. Differentiate between fixed costs and variable costs.

Answer:

Fixed costs:

- Fixed costs are fixed and do not change with the change in output, e.g., expenditure on machines, wages paid to permanent staff.

- Fixed costs can never be zero. They remain the same at all levels of output.

Variable costs:

- Variable costs change with the level of output, e.g., expenditure on raw-material, payment of electricity bill.

- Variable costs become zero when production is stopped.

2. Classify the following into fixed cost and variable cost:

- (a) Rent for a shed

- (b) Minimum telephone bill

- (c) Cost of raw material

- (d) Wages to permanent staff

- (e) Interest on capital

- (f) Payment for transportation of goods

- (g) Telephone charges beyond the minimum

- (h) Daily wages

Answer:

- Fixed cost: (a) Rent for a shed, (b) Minimum telephone bill, (d) Wages to permanent staff, (e) Interest on capital

- Variable cost: (c) Cost of raw material, (f) Payment for transportation of goods, (g) Telephone charges beyond the minimum, (h) Daily wages

3. Can AC fall when MC is rising?

Answer: Yes, AC can fall even when MC is rising. Though MC will necessarily remain below AC when AC is falling, MC may still rise while AC is falling. This happens when the rate at which MC increases is slower than the rate at which AC is decreasing. For example, if an additional unit’s cost (MC) increases slightly, while the total average cost is still falling due to earlier low costs, then AC continues to decrease even though MC is rising.

4. What is meant by explicit cost? Which of the following are included in it?

- (a) Payment of wages to employees of the firm

- (b) Wages for entrepreneur’s own labour

- (c) Depreciation costs

- (d) Rent on entrepreneur’s own building

- (e) Payment of electricity bill

Answer: Explicit cost refers to the actual monetary expenditure on inputs used in production. It includes payments made to outsiders for services provided.

- (a) Payment of wages to employees of the firm

- (c) Depreciation costs

- (e) Payment of electricity bill

The wages for the entrepreneur’s own labour and rent on the entrepreneur’s own building are implicit costs, not explicit costs.

5. Distinguish between explicit costs and implicit costs.

Answer: Explicit costs refer to the actual monetary expenditure on inputs, such as payments made to outsiders for wages, rent, and raw materials. Implicit costs, on the other hand, are the estimated value of inputs supplied by the owner of the firm, such as imputed salary of the owner or imputed rent for the owner’s building. Explicit costs are recorded in the accounting records, while implicit costs are not. Both explicit and implicit costs contribute to the calculation of economic costs.

6. Why does the TC curve start from the Y-axis and TVC curve from the Y-axis?

Answer: The Total Cost (TC) curve starts from the Y-axis because even when output is zero, a firm incurs fixed costs, which are represented on the Y-axis. In contrast, the Total Variable Cost (TVC) curve starts from the origin, as variable costs are incurred only when there is production. When output is zero, variable costs are also zero, hence TVC begins from the origin.

7. Why is average cost curve U-shaped in the short-run? Give reasons.

Answer: The average cost curve is U-shaped in the short run due to the law of variable proportions. Initially, as production increases, the firm experiences increasing returns to scale, which leads to a decline in the average cost. However, beyond a certain point, the firm experiences diminishing returns to scale, causing the average cost to rise. This gives the AC curve its characteristic U-shape.

8. Discuss the relationship between average cost and marginal cost with the help of a diagram.

Answer: The relationship between average cost (AC) and marginal cost (MC) is such that when MC is less than AC, the average cost falls, and when MC is greater than AC, the average cost rises. At the minimum point of the average cost curve, MC equals AC. The marginal cost curve cuts the average cost curve at its lowest point.

9. Explain the relationship between average total cost curve, average variable cost curve and marginal cost curve. (Or) Do ATC and AVC curves intersect each other? Give reasons.

Answer: The average total cost (ATC) curve and average variable cost (AVC) curve are both U-shaped, reflecting the law of variable proportions. The marginal cost (MC) curve also follows a U-shape and intersects both the ATC and AVC curves at their minimum points. As output increases, the gap between the ATC and AVC narrows because the average fixed cost (AFC) diminishes. Therefore, the MC curve intersects the AVC curve before it intersects the ATC curve.

Numerical Questions

1. From the following data given below, calculate (i) Marginal cost and (ii) Average cost.

| Output | Total cost in ₹ |

| 1 | 10 |

| 2 | 20 |

| 3 | 28 |

| 4 | 34 |

| 5 | 38 |

| 6 | 42 |

| 7 | 48 |

| 8 | 56 |

Answer:

| Output | Total cost in ₹ | Marginal Cost (MC) | Average Cost (AC) |

| 1 | 10 | – | 10 |

| 2 | 20 | 10 | 10 |

| 3 | 28 | 8 | 9.3 |

| 4 | 34 | 6 | 8.5 |

| 5 | 38 | 4 | 7.6 |

| 6 | 42 | 4 | 7 |

| 7 | 48 | 6 | 6.8 |

| 8 | 56 | 8 | 7 |

(i) Marginal cost (MC)

- At output 1: There is no previous output, so MC is not defined.

- At output 2: MC = Total cost at output 2 – Total cost at output 1

MC = 20 – 10 = 10 - At output 3: MC = Total cost at output 3 – Total cost at output 2

MC = 28 – 20 = 8 - At output 4: MC = Total cost at output 4 – Total cost at output 3

MC = 34 – 28 = 6 - At output 5: MC = Total cost at output 5 – Total cost at output 4

MC = 38 – 34 = 4 - At output 6: MC = Total cost at output 6 – Total cost at output 5

MC = 42 – 38 = 4 - At output 7: MC = Total cost at output 7 – Total cost at output 6

MC = 48 – 42 = 6 - At output 8: MC = Total cost at output 8 – Total cost at output 7

MC = 56 – 48 = 8

(ii) Average cost (AC)

- At output 1: AC = Total cost at output 1 ÷ Output

AC = 10 ÷ 1 = 10 - At output 2: AC = Total cost at output 2 ÷ Output

AC = 20 ÷ 2 = 10 - At output 3: AC = Total cost at output 3 ÷ Output

AC = 28 ÷ 3 = 9.3 - At output 4: AC = Total cost at output 4 ÷ Output

AC = 34 ÷ 4 = 8.5 - At output 5: AC = Total cost at output 5 ÷ Output

AC = 38 ÷ 5 = 7.6 - At output 6: AC = Total cost at output 6 ÷ Output

AC = 42 ÷ 6 = 7 - At output 7: AC = Total cost at output 7 ÷ Output

AC = 48 ÷ 7 = 6.8 - At output 8: AC = Total cost at output 8 ÷ Output

AC = 56 ÷ 8 = 7

16. Complete the following table:

| Output (units) | AFC (₹) | MC (₹) | TC (₹) |

| 1 | – | 60 | – |

| 2 | 18 | – | 82 |

| 3 | – | – | – |

| 4 | 20 | 120 | 99 |

| 5 | 22 | – | – |

Answer:

| Output (units) | AFC (₹) | MC (₹) | TC (₹) |

| 1 | 60 | 60 | 72 |

| 2 | 30 | 12 | 82 |

| 3 | 18 | 9 | 90 |

| 4 | 15 | 120 | 99 |

| 5 | 12 | 9 | 109 |

Steps:

- (i) Average Fixed Cost (AFC):

AFC = TFC ÷ Output

Assuming TFC = ₹60- For output 1: AFC = 60 ÷ 1 = ₹60

- For output 2: AFC = 60 ÷ 2 = ₹30

- For output 3: AFC = 60 ÷ 3 = ₹18

- For output 4: AFC = 60 ÷ 4 = ₹15

- For output 5: AFC = 60 ÷ 5 = ₹12

- (ii) Marginal Cost (MC):

MC = TC (current output) – TC (previous output)- For output 1: MC is given as ₹60

- For output 2: MC = 82 – 72 = ₹12

- For output 3: MC = 90 – 82 = ₹9

- For output 4: MC is given as ₹120

- For output 5: MC = 109 – 99 = ₹9

- (iii) Total Cost (TC):

- For output 1: TC is given as ₹72

- For output 2: TC = 72 + 12 = ₹82

- For output 3: TC = 82 + 8 = ₹90

- For output 4: TC is given as ₹99

- For output 5: TC = 99 + 9 = ₹109

Extras

Additional MCQs

1. What do explicit costs include?

A. Payments for raw materials

B. Implicit costs

C. Normal profit

D. Rent of self-owned building

Answer: A. Payments for raw materials

19. When is Long-Run Average Cost (LAC) equal to Long-Run Marginal Cost (LMC)?

A. When LAC is rising

B. When LAC is falling

C. At the minimum point of the LAC curve

D. When output is zero

Answer: C. At the minimum point of the LAC curve

Additional questions and answers

1. What is the link between a firm’s output, costs, and revenue?

Answer: The output of a commodity is linked to costs on one hand and revenue on the other. To produce output, a firm must employ inputs, and the payment for these inputs is called cost. The output produced is linked to total revenue in the product market. Production decisions of a firm are guided by its cost and revenue conditions.

23. What is the relationship between Total Cost (TC) and Marginal Cost (MC)?

Answer:

- When TC rises at a diminishing rate, MC decreases.

- When the rate of increase in TC stops diminishing, MC is at its minimum point.

- When TC rises at an increasing rate, MC increases.

MC is calculated from TC as follows:

MC = ΔTC / ΔQ

or

MC = TCᵢ – TCᵢ₋₁.

Get notes of other classes and subjects