Get summaries, questions, answers, solutions, notes, extras, PDF and guide of Class 11 (first year) Economics textbook, chapter 8 Producer’s Equilibrium which is part of the syllabus of students studying under AHSEC/ASSEB (Assam Board). These solutions, however, should only be treated as references and can be modified/changed.

If you notice any errors in the notes, please mention them in the comments

Summary

Chapter 8, titled “Producer’s Equilibrium,” explains how a producer reaches a point where profits are maximized and no changes in output will increase or decrease these profits.

A producer is someone who combines various resources to create goods or services and sell them for profit. Producer’s equilibrium is achieved when the difference between total revenue (TR) and total cost (TC) is maximized. This point means the producer has no motivation to increase or decrease production. The chapter introduces two key methods to find this equilibrium.

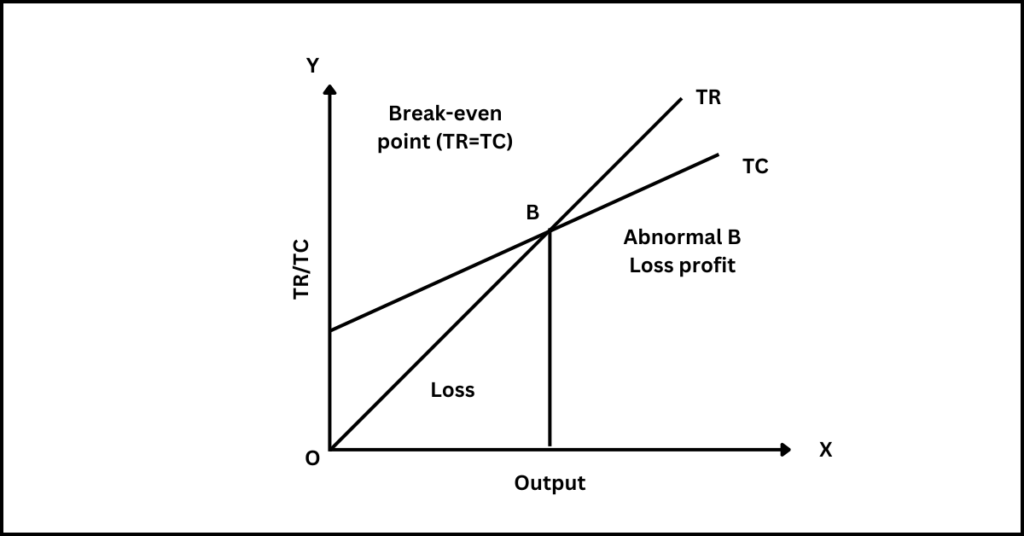

The first method is the Total Revenue and Total Cost Method. According to this, producers reach equilibrium when the gap between TR and TC is widest. A simple example shows that the maximum profit happens when 40 units of a product are made, as the TR minus TC difference is greatest. In a graph, equilibrium occurs where the TC curve meets the TR curve, illustrating the point of maximum profit.

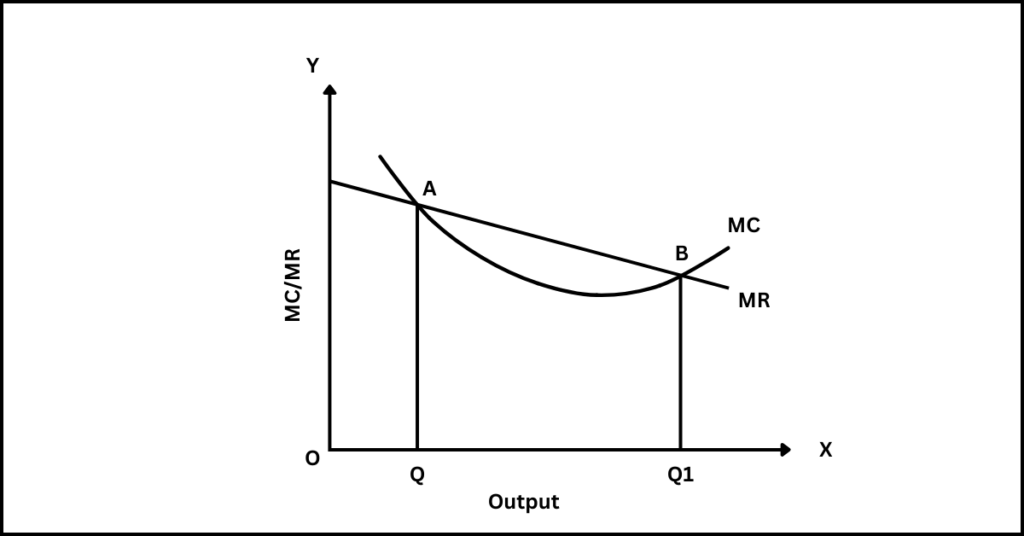

The second method, the Marginal Revenue (MR) and Marginal Cost (MC) Method, explains that equilibrium happens when MR equals MC. MR is the extra revenue from selling one more unit, while MC is the extra cost of making that unit. As long as MR is greater than MC, the producer can increase profits by making more. But when MC becomes greater than MR, any extra production will lower profits. Therefore, equilibrium is reached when MR equals MC, and after that, MC rises above MR, showing the producer should stop increasing production.

The chapter also discusses various market conditions like fixed and changing prices. For example, when prices are fixed, equilibrium is reached at the point where MR equals MC, and MC rises after this point. In another situation, where more units can only be sold at a lower price, the producer reaches equilibrium when MR equals MC and profits are maximized.

The break-even point is when total revenue equals total cost, leading to no profit or loss. If production falls below this point, the firm will face losses, and any output above it results in profit.

The chapter addresses the shutdown point, which occurs when the price of a good is just enough to cover variable costs. If the price falls below this level, the producer should stop production.

Video tutorial

Textbook solutions

Very Short Answer Type Questions

1. How is a firm’s profit measured?

Answer: A firm’s profit is measured by the difference between total revenue and total cost.

2. Does a firm always earn profit when it is in equilibrium?

Answer: No, a firm does not always earn profit when it is in equilibrium. At the break-even point, a firm earns only normal profits, not economic profits.

3. Does equality between MC and MR also mean equality between AC and AR?

Answer: No, equality between MC and MR does not mean equality between AC and AR.

4. What happens if output is increased beyond the equilibrium level?

Answer: If output is increased beyond the equilibrium level, profits will decline because marginal cost will exceed marginal revenue.

Short Answer Type Questions

1. Explain the conditions of producer’s equilibrium with the help of a marginal cost and marginal revenue schedule.

Answer: Producer’s equilibrium is the situation of that level of output which gives the producer maximum profit. At equilibrium point, he has no incentive to increase or decrease the level of output. Two conditions of Producer’s Equilibrium:

(i) MC = MR

(ii) MC should be increasing with output.

2. Will a profit maximizing firm in a competitive market produce a positive level of output in the short run if the market price is less than the minimum of AVC?

Answer: No. A profit-maximizing firm under perfect competition will not produce a level of output in the short run when market price is less than the minimum of AVC. It is because equality between market price and minimum AVC (P-AVC) indicates shut down point. A competitive firm can bear losses maximum up to fixed cost. If P<AVC, it will have to bear losses more than fixed cost. So a firm will not produce a positive level of output if P<AVC in the short run.

3. Explain the conditions leading to maximisation of profits by a producer. Use total cost and total revenue approach.

Answer: A producer will be in equilibrium when the following two conditions are satisfied:

(i) The difference between total revenue and total cost is maximum.

(ii) The marginal cost should equal marginal revenue. This can be explained with the total cost and total revenue approach, where the producer will attain equilibrium when the difference between total revenue (TR) and total cost (TC) is the highest.

Explain producer’s equilibrium using a schedule. Use total cost and total revenue approach.

Answer: Producer’s equilibrium can be explained using the total cost and total revenue approach. The producer will be in equilibrium at that level of output where the difference between total revenue (TR) and total cost (TC) is maximum. Let us take an example to understand this:

| Output (Units) | Price (₹) | TR (₹) | TC (₹) | Profit = (TR – TC) |

|---|---|---|---|---|

| 0 | 10 | 0 | 50 | -50 |

| 10 | 10 | 100 | 100 | 0 |

| 20 | 10 | 200 | 150 | 50 |

| 30 | 10 | 300 | 200 | 100 |

| 40 | 10 | 400 | 310 | 90 |

In the above example, the maximum profit of ₹100 is achieved by producing 30 units. Therefore, the producer will be at equilibrium at 30 units of output because at this level both conditions of equilibrium are satisfied: (i) MC = MR, (ii) MC is rising after MC = MR output.

4. Explain why MC=MR is the profit maximisation principle of a firm in general.

Answer: The profit maximisation principle for a firm is that marginal cost (MC) should equal marginal revenue (MR). This is because when MC = MR, the firm maximises its profit by producing the optimum level of output. If MC is less than MR, the firm can increase profit by increasing output. On the other hand, if MC is greater than MR, the firm should reduce output to maximise profit. Therefore, the equality of MC and MR is the key condition for profit maximisation.

5. Find the level of output at which the producer will be in equilibrium. Give reasons for your answer.

Answer: The producer will be in equilibrium at that level of output where marginal cost (MC) is equal to marginal revenue (MR) and marginal cost is rising after equilibrium. The equality between MC and MR is a necessary condition but not a sufficient condition for equilibrium. The second condition is that MC must be rising after equilibrium, as producing beyond the equilibrium point would lead to a decline in profits. Therefore, the level of output where both conditions are satisfied is the equilibrium level of output.

6. Distinguish between normal profits and supernormal profits.

Answer: Normal profits are the minimum profit that the producer expects from his capital invested in the business. If this minimum profit is not available, he will withdraw his capital from the existing use and shift it to the next best alternative use cost of production. Just as wages paid to labour, interest to capital rent paid to the owner’s factory building are included in cost of production normal profits are a part of cost of production. In a situation of normal profit, price is just equal to average cost of production. Normal profits are a part of cost of production.

On the other hand, supernormal profits also called abnormal profits are the profits over and above the normal profits. These profits are likely to attract the entry of new firms. If at equilibrium point, price is greater than average cost of production it is referred to a situation of supernormal profits.

Long Answer Type Questions

1. Why must MC be rising at the point of producer’s equilibrium? Explain.

Answer: Marginal cost (MC) must be rising at the point of producer’s equilibrium because equilibrium requires not only that MC equals marginal revenue (MR), but also that producing more beyond this point would reduce profits. If MC is rising after the point of equality, it ensures that any further increase in output would result in higher costs than revenue, leading to a decrease in profit. This rising MC condition ensures that the producer has reached the profit-maximizing level of output and cannot increase profit by producing more.

2. What is producer’s equilibrium? Explain the conditions of producer’s equilibrium through the ‘marginal cost and marginal revenue’ approach. Use diagram.

Answer: Producer’s equilibrium refers to the level of output at which a producer maximizes profits. This occurs when two conditions are satisfied:

- Marginal Cost (MC) equals Marginal Revenue (MR).

- MC is rising at the point where MC equals MR.

In this approach, the producer adjusts output until the extra cost of producing one more unit (MC) equals the extra revenue from selling that unit (MR).

A producer is not in equilibrium if MC is less than MR because producing more would increase profits. Similarly, if MC is greater than MR, reducing output would increase profits. Therefore, equilibrium is achieved when MC equals MR, and MC must be rising after that point to ensure maximum profit.

In the diagram, output is shown on the x-axis, and revenue and costs are on the y-axis. The MC curve is U-shaped and cuts the MR curve at two points, but equilibrium is achieved only when the MC curve is rising after crossing the MR curve.

3. Define producer’s equilibrium. Explain the conditions of producer’s equilibrium in terms of total cost and total revenue. Use diagram.

Answer: Producer’s equilibrium is defined as the level of output at which a producer maximizes profit. This is where the difference between total revenue (TR) and total cost (TC) is the greatest.

There are two main conditions for producer’s equilibrium in terms of total cost and total revenue:

- The difference between TR and TC should be maximum.

- At this level, the producer has no incentive to change the level of output as it would reduce profit.

In the diagram, output is represented on the x-axis, while TR and TC are on the y-axis. TR and TC curves are drawn, and the producer is in equilibrium at the point where the vertical distance between the TR and TC curves is the maximum. This is the point where profits are the highest.

4. Explain the position of producer’s equilibrium when a firm (producer): (a) is able to sell more quantity at the same price; (b) is able to sell more quantity of output only by lowering the price.

Answer: (a) When a firm is able to sell more quantity at the same price, the AR (Average Revenue) curve is horizontal and MR (Marginal Revenue) equals AR. The producer will be in equilibrium where MC equals MR, and MC is rising after that point. In a perfectly competitive market, where the firm can sell additional output without lowering the price, the MR remains constant. The equilibrium output is determined at the point where the MC curve intersects the MR curve from below. This is the profit-maximizing output level.

(b) When a firm is able to sell more quantity of output only by lowering the price, the AR curve is downward sloping, and MR lies below AR. In this case, equilibrium occurs where MC equals MR, and MC must be rising after this point. As the price decreases with additional output, MR also falls, so equilibrium is achieved where the MR curve intersects the rising portion of the MC curve. Producing beyond this point would result in MC exceeding MR, thus reducing profits. Therefore, the firm is in equilibrium where these two conditions are met.

5. From the following schedule find out the level of output at which the producer is in equilibrium. Give reasons for your answer.

Answer:

| Output (Units) | Price (₹) | Total Cost (₹) | Marginal Cost (₹) | Marginal Revenue (₹) |

|---|---|---|---|---|

| 1 | 24 | 26 | – | – |

| 2 | 24 | 50 | 24 | 24 |

| 3 | 24 | 72 | 22 | 24 |

| 4 | 24 | 92 | 20 | 24 |

| 5 | 24 | 115 | 23 | 24 |

| 6 | 24 | 139 | 24 | 24 |

| 7 | 24 | 165 | 26 | 24 |

(i) Find Marginal Revenue (MR):

Since the price per unit is ₹24 and remains constant, the marginal revenue is ₹24 for all levels of output.

(ii) Find Marginal Cost (MC):

The Marginal Cost (MC) is calculated as the change in total cost when one more unit of output is produced.

For output = 1, MC = N/A (since we do not have previous output data).

For output = 2, MC = ₹50 – ₹26 = ₹24.

For output = 3, MC = ₹72 – ₹50 = ₹22.

For output = 4, MC = ₹92 – ₹72 = ₹20.

For output = 5, MC = ₹115 – ₹92 = ₹23.

For output = 6, MC = ₹139 – ₹115 = ₹24.

For output = 7, MC = ₹165 – ₹139 = ₹26.

(iii) Apply the equilibrium condition (MC = MR):

The producer is in equilibrium when marginal cost (MC) equals marginal revenue (MR). From the table, we observe that MC = MR at 6 units of output, where both MC and MR are ₹24.

Thus, the producer is in equilibrium at 6 units of output.

6. Given below is a cost and revenue schedule of a producer. At what level of output is the producer in equilibrium? Give reasons for your answer.

| Output (Units) | Price (₹) | Total Cost (₹) | Marginal Cost (₹) | Marginal Revenue (₹) |

|---|---|---|---|---|

| 1 | 10 | 13 | – | – |

| 2 | 10 | 22 | 9 | 10 |

| 3 | 10 | 30 | 8 | 10 |

| 4 | 10 | 38 | 8 | 10 |

| 5 | 10 | 47 | 9 | 10 |

| 6 | 10 | 57 | 10 | 10 |

| 7 | 10 | 71 | 14 | 10 |

Answer:

(i) Find Marginal Revenue (MR):

Since the price per unit is ₹10 and remains constant, the marginal revenue is ₹10 for all levels of output.

(ii) Find Marginal Cost (MC):

For output = 1, MC = N/A.

For output = 2, MC = ₹22 – ₹13 = ₹9.

For output = 3, MC = ₹30 – ₹22 = ₹8.

For output = 4, MC = ₹38 – ₹30 = ₹8.

For output = 5, MC = ₹47 – ₹38 = ₹9.

For output = 6, MC = ₹57 – ₹47 = ₹10.

For output = 7, MC = ₹71 – ₹57 = ₹14.

(iii) Apply the equilibrium condition (MC = MR):

The producer is in equilibrium when marginal cost (MC) equals marginal revenue (MR). From the table, we observe that MC = MR at 6 units of output, where both MC and MR are ₹10.

Thus, the producer is in equilibrium at 6 units of output.

7. On the basis of the information given below, determine the level of output at which the producer will be in equilibrium. Use the marginal cost – marginal revenue approach. Give reasons for your answer.

| Output (Units) | Average Revenue (₹) | Total Cost (₹) | Marginal Cost (₹) | Marginal Revenue (₹) |

|---|---|---|---|---|

| 1 | 7 | 7 | – | – |

| 2 | 7 | 15 | 8 | 7 |

| 3 | 7 | 22 | 7 | 7 |

| 4 | 7 | 28 | 6 | 7 |

| 5 | 7 | 33 | 5 | 7 |

| 6 | 7 | 40 | 7 | 7 |

| 7 | 7 | 48 | 8 | 7 |

Answer:

(i) Find Marginal Revenue (MR):

Since the average revenue is ₹7 and remains constant, the marginal revenue is ₹7 for all levels of output.

(ii) Find Marginal Cost (MC):

For output = 1, MC = N/A.

For output = 2, MC = ₹15 – ₹7 = ₹8.

For output = 3, MC = ₹22 – ₹15 = ₹7.

For output = 4, MC = ₹28 – ₹22 = ₹6.

For output = 5, MC = ₹33 – ₹28 = ₹5.

For output = 6, MC = ₹40 – ₹33 = ₹7.

For output = 7, MC = ₹48 – ₹40 = ₹8.

(iii) Apply the equilibrium condition (MC = MR):

The producer is in equilibrium when marginal cost (MC) equals marginal revenue (MR). From the table, we observe that MC = MR at 6 units of output, where both MC and MR are ₹7.

Thus, the producer is in equilibrium at 6 units of output.

Extra

Additional MCQs

1. What does a producer aim to achieve through production?

A. Maximize sales

B. Maximize output

C. Maximize profit

D. Maximize revenue

Answer: C. Maximize profit

10. In which method is a firm in equilibrium when the difference between total revenue and total cost is maximized?

A. Marginal Revenue and Marginal Cost Method

B. Total Revenue and Total Cost Method

C. Average Revenue and Total Cost Method

D. Marginal Cost and Total Profit Method

Answer: B. Total Revenue and Total Cost Method

Additional questions and answers

1. Who is a producer?

Answer: A producer (or a firm) is a person or economic entity who produces and sells a commodity or service. In the process of production, the producer utilizes various factors of production (also called resources). The goal of production for a producer is to earn profit.

Q. What is meant by producer’s equilibrium?

Answer: A producer’s equilibrium occurs when the producer maximizes their profit. In other words, the producer reaches a level of output that provides the maximum profit. At this level, there is no incentive to increase or decrease production. Profits, denoted by the Greek letter π (pi), are maximized when the difference between total revenue (TR) and total cost (TC) is the greatest. Therefore, π = TR – TC. In short, a producer is in equilibrium when the difference between total revenue and total cost is at its maximum.

Q. How is the position of producer’s equilibrium determined in a perfectly competitive market?

Answer: In a perfectly competitive market, the price of a product is determined by the forces of demand and supply. Each firm in this market is a price-taker, while the market or industry sets the price. The firm’s average revenue remains the same across all output levels and coincides with marginal revenue. The total revenue curve of the firm is an upward-sloping straight line, which means total revenue increases proportionally with output.

There are two methods for determining producer’s equilibrium:

- Total Revenue and Total Cost Method

- Marginal Revenue and Marginal Cost Method

Q. What is the Marginal Revenue and Marginal Cost method of determining producer’s equilibrium?

Answer: The Marginal Revenue and Marginal Cost method states that a producer is in equilibrium when:

- MC = MR: This means that marginal cost (MC) equals marginal revenue (MR). MC is the addition to total cost when one more unit of output is produced, and MR is the addition to total revenue from selling one more unit.

- MC is greater than MR after the equilibrium point: It ensures that producing beyond the equilibrium point will reduce profits. Therefore, equilibrium is achieved only when MC equals MR and MC rises after that point.

Q. How does a producer achieve equilibrium when price remains fixed?

Answer: In a competitive market where price is fixed, the producer’s equilibrium is achieved when two conditions are met:

- MC = MR

- MC becomes greater than MR after the equilibrium point.

Q. How does a producer achieve equilibrium when the price is variable?

Answer: When the price is variable, a producer achieves equilibrium by ensuring:

- MC = MR

- MC must be rising at the equilibrium point.

Q. What is the relationship between price and marginal cost at equilibrium output?

Answer: Price and marginal cost are equal at equilibrium output when price remains constant because price (or AR) is equal to MR. Since, at equilibrium, MC = MR and price equals MR, it follows that P = MC. Price can neither be greater nor less than marginal cost at equilibrium for a firm in a competitive market. However, if more output is sold only by reducing the price, then price (or AR) becomes greater than MR. As equilibrium is attained when MC = MR, this means that P > MC at the equilibrium output level.

Q. What are normal and supernormal profits?

Answer:

- Normal Profits: Normal profits are the minimum profits that a producer expects from the capital invested in the business. If these minimum profits are not available, the producer will withdraw the capital and shift it to the next best alternative use. Normal profits are included in the cost of production, just like wages for labour, interest on capital, and rent for the factory building. In a situation of normal profit, the price is just equal to the average cost of production, making normal profits a part of production cost.

- Supernormal Profits: Supernormal profits, also called abnormal profits, are the profits earned over and above normal profits. These profits are likely to attract the entry of new firms. If, at equilibrium, the price is greater than the average cost of production, it leads to a situation of supernormal profits.

Q. What is the break-even point?

Answer: The break-even point refers to a situation where a firm’s total revenue equals total costs, or where average revenue equals average cost. It is the specific level of output or sales where the firm breaks even, meaning total costs are just equal to total revenue. At the break-even point, the firm incurs neither losses nor profits. If the firm produces and sells less than the break-even point, it will incur losses; if it produces and sells more, it makes profits. Therefore, the break-even point represents the minimum level of production or sales required for the firm to be economically viable.

Q. What is the shut-down point, and when should a firm stop production?

Answer: The shut-down point is the level of output where total revenue equals total variable cost (TR = TVC) or where average revenue equals average variable cost (AR = AVC). A firm should continue producing in the short run if the price is greater than the average variable cost at equilibrium output. The firm covers its variable costs fully and a part of its fixed costs. The shut-down point indicates the loss-minimising condition, and a firm will stop production in the short run if the market price goes below the point where total revenue covers only variable costs.

The shut-down point satisfies three conditions:

(a) MC = MR

(b) MC must be rising at the equilibrium point

(c) P ≥ AVC

At the shut-down point, the firm incurs a loss equal to its fixed costs.

Q. What are the conditions a firm must satisfy to continue producing despite making losses?

Answer: A firm should continue production in the short run if the following conditions are satisfied:

(a) Marginal cost (MC) equals marginal revenue (MR)

(b) Marginal cost (MC) must be rising at the equilibrium point

(c) The price (P) is greater than or equal to average variable cost (AVC)

If these conditions hold, the firm should continue production even if it incurs some losses, as long as it covers variable costs and a part of fixed costs.

Q. Explain the significance of the shut-down point.

Answer: The shut-down point represents the level of output where the firm’s total revenue is equal to its total variable cost (TR = TVC) or where average revenue equals average variable cost (AR = AVC). At this point, the firm is only covering its variable costs, and any price below this level would cause the firm to shut down in the short run.

[/um_show_content]

[/um_loggedin]

14. When does a firm earn only normal profits?

Answer: A firm earns only normal profits at the break-even point, where total revenue equals total cost (TR = TC) and the difference between the two is zero. At this point, the firm’s output level ensures that no economic profit is earned, and the firm covers all costs, including normal profits, which are a part of production costs.

Get notes of other boards, classes, and subjects